Insurance exists to protect you from huge bills after accidents, damage, or illness. But getting that dreaded denial letter can feel like a punch to the gut. But the good news is that denial is not the end of the road. Many rejected claims can be approved with the right approach. The key is to act fast, stay super organized, and put everything in writing. Communications should not be made by phone, as they can be forgotten or misinterpreted later.

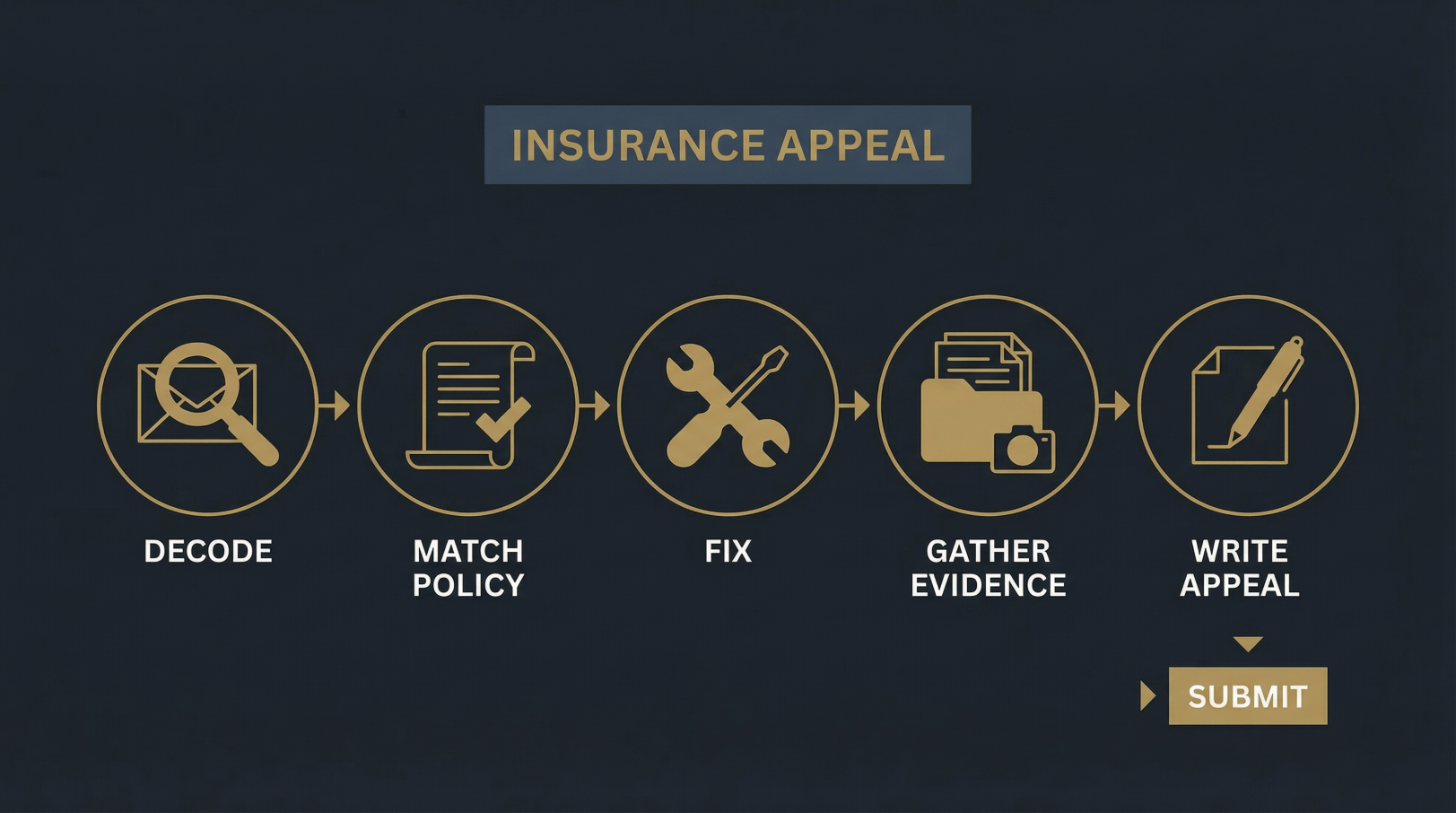

First: Decode That Denial Letter

First, review the denial letter as a detective would. Find out what exact reason they give? Look for missing details, such as dates, policy sections, and forms they requested but didn’t receive. Figure out if the explanation is fuzzy. Then call and request a clearer, written explanation right away.

And most importantly: circle any deadlines for appeals. Insurance companies often give you a tight window to respond. If you miss it, you might lose your chance forever. Also, note any “next steps” they mention or extra documents they need.

Match the Denial to Your Actual Policy

The next step is to pull out your insurance policy. It is the boring document you probably never read when you signed up for the policy. Find the exact section that covers your situation. Look at all the limits, exclusions, waiting periods, and steps you need to follow.

Common reasons claims are denied include: requesting more than your plan covers, receiving treatment deemed “not medically necessary,” losing coverage after missed payments, or seeing an out-of-network doctor without prior approval. Your policy lists these rules clearly. If you miss one, the claim can fall apart fast.

Fix What Went Wrong

There are many mistakes you can fix to avoid claim denials. Were you too late in filing? Did we send an incomplete form? Were there mistakes in the paperwork? Insurance companies are known to deny claims even for minor errors.

Another big problem is not getting pre-approval when needed or seeing the wrong doctors. Also, don’t forget the proof factor. Insurance companies need proof of everything. It is not enough to tell them. You need hard evidence.

Build a Rock-Solid Evidence Package

Create a folder labeled with your claim number, policy, denial letter, and all company emails. Then add every piece of evidence that supports your case.

For property damage, include clear photos/videos, repair estimates, and actual bills. If you are injured, gather all medical records and itemized bills. If you are missing work, you can add your pay stubs and a letter from your boss confirming the days you missed.

Pro tip: Send documents in a logical order. Label everything clearly. Make it very easy for the claims person to see why you deserve coverage.

Put Your Appeal in Writing

Follow the insurer’s appeal rules exactly. Write a clear letter that explains:

- What happened (brief but complete)

- What you’re asking for

- Why your policy should cover it

- A neat list of all documents attached

You should not rely solely on phone calls. They’re too easy to forget or misinterpret. Always request written confirmation that they received your appeal, and ask when you can expect a response.